Your premium just went up. Maybe it happened at renewal without much explanation. Maybe you got a letter and the number was bigger than last year and you are not sure why. So now you are shopping — and you are wondering whether putting your home and auto with one agent is actually worth it or just a convenience pitch.

Here is what most people miss in that process: they go looking for a lower number. What they actually need is someone to audit what they have.

What “Home and Auto With One Agent” Actually Means

People do not usually say they want a “bundle.” They say they want their home and auto with one agent — one call when something goes wrong, one person who knows their whole picture, no situation where two separate companies are pointing at each other after a claim.

That is the real value here. Not a discount percentage. A relationship with someone who is actually responsible for making sure you are protected.

David puts it this way:

“I don’t like to have policyholders. I like to have clients who are insured. Bring me everything — let me insure everything so I know there are no gaps in your coverage. That way I know you’re protected and you can deal with the more important things in life.”

That is a different philosophy than most agencies operate on. Most agents quote what you already have at a lower price. That is not an audit. It is a transaction.

When your home and auto are with one agent who has seen your full picture — your roof age, your cars, your household situation — that agent can actually catch the gaps. The coverage you dropped to save $40 a month two years ago. The liability limit that made sense in 2018 and does not make sense now. The policy your last agent never questioned because you never asked.

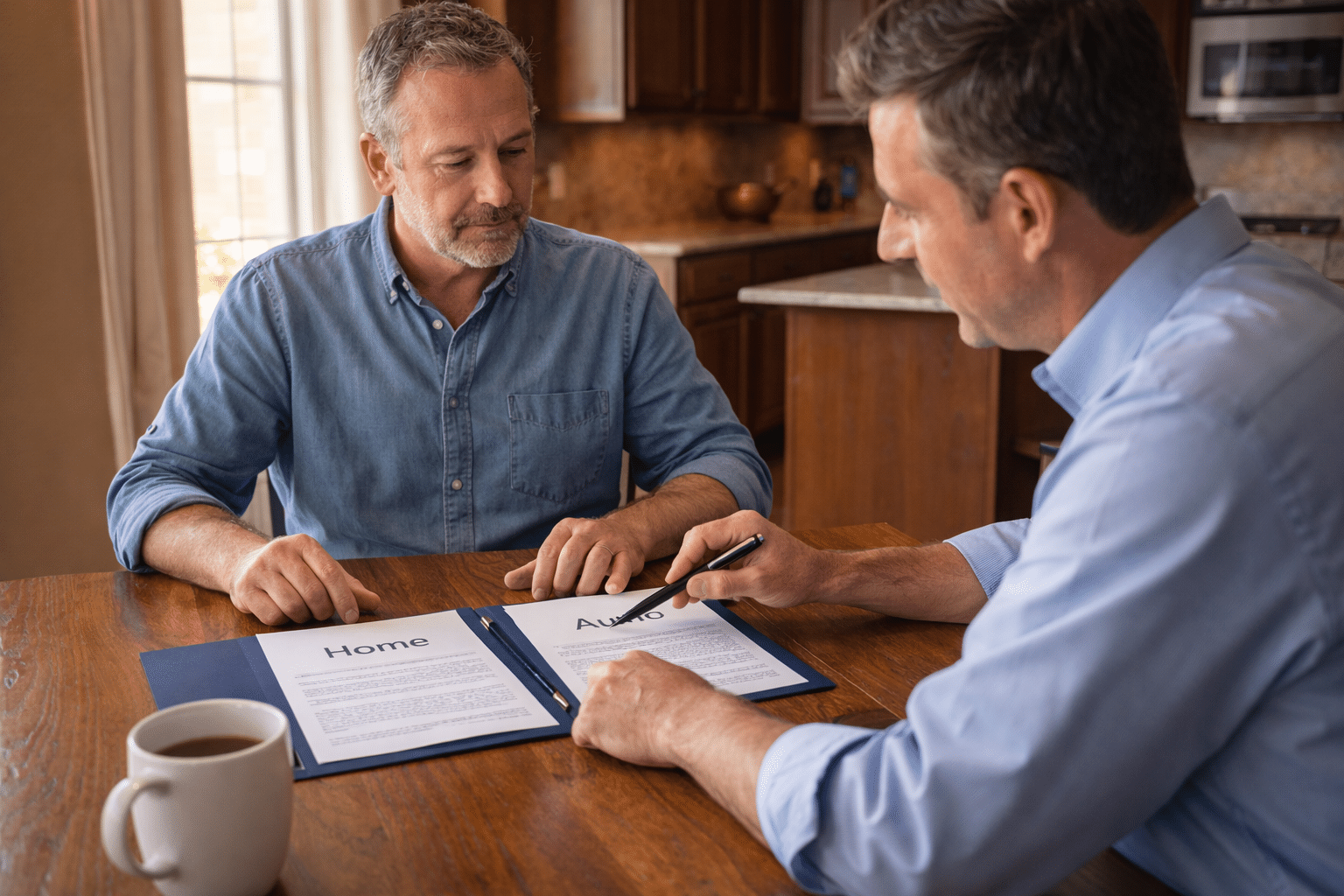

The Discount Stack: What Actually Changes When You Put Policies Together

The financial case for having your home and auto with one agent is real. Here is how it layers:

Multi-policy discount — both directions. When you carry home and auto with the same carrier, you typically get a multi-policy discount applied to both policies — not just one. The home gets cheaper. The auto gets cheaper. That is two lines moving in your favor at once.

Life insurance adds another layer. If you add a life insurance policy into the mix, many carriers stack an additional discount on top. Three policies with one carrier often earns more than double the discount of two.

Occupation discounts most agents never ask about. Some carriers extend agent-level discounts to certain occupations — teachers, nurses, firefighters, and others. These are legitimate carrier discount programs, and they only get applied if your agent knows to ask. Most do not.

The checklist nobody else runs. When you call our office, the first conversation is not about your current premium. It is about your situation. Roof age. Whether you have a vacation property or a rental. What you do for work. Who referred you. This is not small talk — it is the process for finding every discount you qualify for before we ever quote a number.

With two degrees in economics, David understands how insurance pricing models actually work — and he uses that to find where you’re being overcharged.

What Actually Happens When You Call

Most agents pull your current policy and requote it at a slightly lower number. That is the industry standard pitch. You get a cheaper version of what you already have.

That is not what happens here.

When you call, the first step is an audit — not a requote. David runs through a checklist on every new client conversation:

- Roof age. This is the single biggest driver of home insurance pricing in Texas right now. A roof over a certain age changes your options significantly. Knowing this upfront means no surprises.

- Occupation. Firemen, nurses, teachers, and other professions qualify for discounts at certain carriers that most policyholders never receive — because most agents never ask.

- Vacation or secondary property. If you have a lake house, a rental, or a second property anywhere, that needs to be on the radar. Coverage gaps between properties are real.

- Who referred you. David always asks. Sometimes the referral source reveals a discount opportunity. Always it tells him something about what kind of client he is talking to.

- Rapport before numbers. The conversation comes before the quote. It is not a speed run to a premium number. It is a real conversation about what you actually need.

The result: you do not just get a lower price. You get the right coverage, priced correctly, with no gaps your last agent left behind.

“We Never Quote the Minimums”

There is a race to the bottom in the insurance industry. Agents know they can win business by showing you the lowest number — and the lowest number always comes from cutting limits.

David does not play that game.

“Anybody can throw you a price on the lowest minimum limits. But here’s the truth: no matter how much I dial down your coverages, the amount your premium drops is surprisingly small. So we never quote the minimums. We quote the top limits — and people are always surprised at how little more it costs to have a lot more coverage.”

This matters because the difference between minimum coverage and real coverage is enormous if something serious happens — but the difference in premium is often not. Customers who see that comparison for the first time are almost always surprised. They assumed higher limits meant significantly higher premiums. The reality is different.

If you have only ever been quoted the minimum, you have never actually seen what real coverage costs. That is worth knowing before your next renewal.

Who This Is For

If your premium just went up: You are the primary audience for this post. You are shopping, you are frustrated, and you want someone to actually explain what you are paying for. That is exactly the conversation we have with every new client. Bring your current policy. We will go through it.

If you just bought a home: Your lender required homeowners insurance. You bought it, maybe in a hurry, maybe through whatever the lender suggested. You still have your auto somewhere else. Rolling both into one place — with a real audit of both policies — is one of the highest-value things a new homeowner can do in their first year. Most do not. You should.

If you are tired of managing two separate agents: When your home claim and your auto claim involve the same incident — a tree falls through your garage door and damages your car, for example — having two separate agents and two separate carriers complicates that process significantly. One agent who knows your whole picture removes that complication entirely.

Ready to See What You Are Actually Paying For?

You do not need to know what you want before you call. You just need to bring what you have.

We will run through your current coverage, tell you what looks right and what does not, and show you what full coverage actually costs compared to what you are carrying now. Most people are surprised in both directions — by the gaps they did not know they had and by how little it costs to close them.

We also send every new client a signed copy of our book, Understanding Insurance in Simple English — no charge. It is the same book David wrote to cut through the jargon that most agents hide behind. You can find it on Amazon if you want to read it before you even call.

Ready to review your current coverage? Request a policy review — no pressure, no obligation.

David Offutt is a licensed insurance agent (TX License #1465807) based in Fort Worth, TX. He holds an MS in Economics and is the co-author of Understanding Insurance in Simple English. He is the founder of Texas Real Estate Academy, where he teaches insurance continuing education to Texas real estate agents. He has earned 138 five-star Google reviews from Fort Worth clients.Frequently Asked Questions

Does bundling home and auto always save money in Texas?

Not always — it depends on your carrier, your risk profile, and what discounts you already carry. In most cases, having home and auto with the same carrier does lower the total premium on both policies. But the bigger value is the audit that comes with it. A good agent finds discount stacks most people have never been offered — occupation discounts, loyalty credits, and coverage adjustments that make the total picture better, not just cheaper.

Can I bundle if my home and auto are currently with different companies?

Yes. Moving both policies to the same carrier is a straightforward process. The right time to do it is usually at one of your renewal dates, so you are not leaving coverage mid-term. We time it to minimize any fees or gaps and make the transition clean.

What other policies can I add to a bundle?

Life insurance is the most common addition and often adds another discount layer on top of the multi-policy discount you already get for home and auto. Renters insurance, umbrella policies, and secondary property coverage can also fold in depending on your situation. The more we know about your household, the better we can find what qualifies.

How do I know if I am currently underinsured?

The most common sign is that you have never had anyone question your limits. If your last agent quoted your current policy and moved on, no one has actually reviewed whether your coverage keeps pace with your home’s current replacement cost, your income, your assets, or your liability exposure. A review takes about 15-20 minutes. Most clients find at least one gap they did not know was there.